This is going to be a short article. On February 23rd, Globe reported solid improvement for the half year ended December 31, 2015. But I don’t have much to tell you in terms of what they did better or how because it wasn’t in the public information. Let’s go with what we’ve got. The numbers are in Australian dollars.

Revenue rose 19.5% to $78.8 million from $66.0 million in last year’s six months (the prior calendar period- PCP). There’s no cost of goods sold provided as there would be in the U.S.

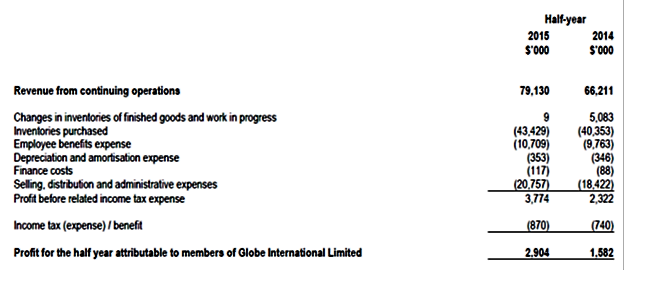

Okay, I think maybe I’ve figured it out with a little help from people who understand the presentation of Australian financial statements better than I do.

They’ve got a line in their income statement (see below) for “Changes in inventories of finished goods and work in progress.” That’s what they use to take into account the change in the existing inventory during the accounting period. During the first six months last year, the amount was $5.083 million. If we subtract that amount from the inventory purchases also shown on the income statement, we get a cost of goods sold of $35.27 million for last year’s six months. For the six months ended December 31, 2016, COGS is $43.42 million.

Sales were $66.211 million during last year’s six months. Subtracting $35.27 million COGS from that gives us a gross profit of $26.94 million and a gross profit margin of 40.7%.

Performing the same calculation for the six months ending December 31, 2015 gives a comparable gross margin of 45.1%. Impressive increase. It would be nice to understand how currency changes impacted that.

I also want to say that I’m not certain whether or not the COGS calculation is the same as it would be in the U.S. But the comparable year over year change is accurate.

Now, let me share with you the summary income statement.

Expenses seem to be in line with revenue growth, and there’s a nice increase of 83.6% in the bottom line.

Reported revenues in Australia rose 36% from $26.3 to $35.7 million, “…with all branded divisions in Australia contributing.” Europe’s sales were flat as reported at $18.6 million. They fell 4% in local currency “…as a result of hardgoods sales falling in this region…” North American were up 16% as reported (let’s hear it for the strong U.S. dollar) from $21.3 to $24.8 million. They fell 6% in local currency “…after a softening of retail in the USA in the second quarter of the financial year.”

Progress at the EBITDA level came almost exclusively from the Australian results. There, EBITDA rose 57% from $3.49 to $5.47 million. The EBITDA loss in North America grew from $1.83 to $2.30 million. Europe’s EBITDA rose just 5.8% from $3.5 to $3.7 million.

They tell us that the “…revenue and profitability improvement was a consequence of recent investments and diversifications into new markets and brands.” They also note that, “Branded highlights included Globe apparel which continued to grow in all regions, work-wear brand FXD and Australia’s 4Front division.”

My guess is that the Globe apparel is bigger than I thought as it’s a brand they choose to mention. Growth is mostly in Australia. Softness in the U.S. isn’t much different from other brands. Strategically, it looks like they get a lot of credit for having the foresight to start FXD and 4Front (their distribution company).

Year over year changes in the balance sheet seem pretty consistent with their growth. I note that their cash flow from operating activities went from a positive $630,000 in the PCP to a negative $6.9 million. “The utilisation of cash during the half year is principally a result of increased investment in working capital to facilitate continuing sales growth and to fund the $1.7 million 2015 final dividend paid October 2015.” Current borrowings on their balance sheet that grew from zero to $5.3 million.

At time when most companies I write about have a focus on controlling expenses and improving their systems, logistics, and supply chains in a low growth environment, Globe is growing it’s business. Not, apparently, across all brands and regions. Still, I’ll take improvements in revenue and net income anytime and anywhere I can get them.

Globe is a public company, but closely held by the Hill brothers, and not followed much by the analysts (note no conference calls) in recent years. I’m guessing this has meant they haven’t had the same conflict between public market driven growth requirements and good branding other companies have suffered from, and have had more flexibility in how they positioned and grew theirs company as a result. Among other things, that means no overly aggressive distribution that damages the brands. I imagine it’s also been easier to take a longer term view.