It’s the financial statements we’re seeing and will see in the next month or so that will begin to help us decide who might be long term winners and speculate on why. I emphasize “speculate” because it’s too soon to reach conclusions. But I begin to think that keeping the new customers you got when competitors were closed or went out of business will be an indicator of success.

Being Essential

In the quarter that ended June 28th, Big 5 Sporting Goods had revenue of $228 million, down just 5.4% from $241 million in last year’s quarter. Gross margin rose from 30.34% to 31.67% while SG&A expense declined by 10.2% to $58.3 million from $73.1 million in last year’s quarter.

Pretax income rose from $200,000 to $15.6 million, a pretty significant increase.

Wait- isn’t there a pandemic or something that clobbered a lot of industry revenues? It depends partly on when your quarter ends for sure. But it surely doesn’t hurt if you’re able to be called “essential” in the jurisdictions where you do most of your business. That’s what Big 5 was able to do.

Timing matters. Big 5 closed half it’s stores beginning March 20. By June 28 they were all open for in store shopping. They never had to close them all. Their quarter started April 1. “The Company was subsequently able to gradually reopen its store locations based on initially qualifying as an “essential” business under applicable regulations and later as a result of the easing of regulatory restrictions on retail operations in the Company’s market areas.” 52% of it’s 421 stores are in California.

One caveat- I don’t have a calculation for how many of their stores were open when competitors weren’t and for how long.

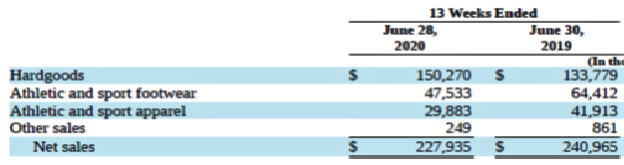

Below is a breakdown of Big 5’s sales for this year’s and last year’s quarter by category (thousands of $).

Go to Big 5’s web site, look at what they sell, and decide for yourself what makes them essential. A little research makes me believe it’s firearms sales, though I’m not sure of that. As you see, hardgoods sales was what kept their revenue decline low.

The balance sheet seems solid. Cash is up from a year ago. Inventory is down 15%. Payables are down, long term debt has been cut in half and equity has risen from last year’s quarter by 6.7% to $186.6 million. Net cash provided by operating activities was $58.3 million, up from $5.6 million in last year’s quarter.

E-commerce Is Important, Right?

Their 10-Q notes that “Revenue associated with e-commerce sales was not material for the 13 and 26 weeks ended June 28, 2020 and June 30, 2019.” I guess I’ve been warming up to the idea that most industry companies had big increases in ecommerce while their stores were closed and that it was important even before the virus was visited on us. But not for Big 5? I wonder why.

No Change in Strategy? Really?

During the conference call (where no analysts chose to be present to ask questions) They referred to the “…fundamental operating principals that have guided Big 5 for over 60 years.” These, they tell us, are convenience, service, value and selection. Management suggests they are more relevant as people try to adjust to the pandemic.

“Our emphasis on customer service and new safety protocols help customers more safely shop our stores and quickly find the products they are looking for. We have built a long-standing reputation in our markets for delivering value at compelling price points and that reputation has continued to resonate with customers throughout the COVID-19 pandemic, particularly given the financial challenges that so many are facing right now and perhaps most important to our recent success is our product selection.”

It’s probably true that their price points are particularly attractive in current economic conditions. Their fundamental operating principals are reasonable, indeed required. But I don’t see them as a distinctive source of competitive advantage. Let’s dig a little deeper.

Possible Short-Term Advantages

Same store sales for the quarter were down 4.2% from last year’s quarter. In the first half of this year’s quarter, they fell 28.2%. In the second half of the quarter, they increased by 15.5% resulting in the 4.2% increase for the whole quarter.

They note that “…as we began reopening stores, we recognized significant shifts in consumer demand and rapidly evolved our product assortment…” Was Big 5 able to take advantage of other retailers cancellations or delays to “evolve” their product offerings at better prices?

Meanwhile, they took “…measures to reduce expense across the organization, including negotiating lease concessions with landlords that would reduce or defer our lease-related payments [$3 million], scaling back merchandise inventory orders and extending payment terms…reducing a significant amount of our workforce…, and reducing advertising and the amount of planned capital spending in fiscal 2020, among other measures.”

Then they continue, “Although a certain portion of these operating expense savings will only benefit the second quarter of fiscal 2020, we expect aspects of these operating expense savings to continue beyond the period.” No mention of how much of which savings are expected to continue.

We do find out that the big increase in the quarter’s net income compared to the same quarter last year “…primarily reflected initiatives that we implemented in response to the COVID-19 pandemic…” Big 5 also improved its merchandise margins by 1.73% over last year’s quarter due to “…a significant shift in our product sales mix towards higher-margin products in May and June of fiscal 2020, as well as lower promotions, as a result of changing consumer demand related to COVID-19.”

Higher margins products are hard goods, as we saw in the chart above. Lower promotions partly because competitors weren’t open for some or part of the quarter? Don’t know.

The conference call reports that July same store sales were up 31.9%. Merchandise margins are up 2% compared to last July. “…we are generating these results while operating our stores with fewer hours and with substantially reduced advertising,” management says in the conference call.

So- what do we do with this? Management gets credit for a great quarter. They made timely decisions in reacting to business conditions changing overnight. It was also good to be declared “essential.” In future quarters, we’ll find out how much of this momentum can be maintained. Is Big 5 taking advantage of an opportunity to evolve it’s business model or are they just making good tactical decisions in a difficult time?

Their continued reliance on 60-year-old fundamental operating principals that don’t seem distinctive and lack of “significant” ecommerce business makes me think the later. The results for the quarter and into July make me hope it’s the former.