Deckers is mostly of interest to us because of their ownership of Sanuk. We’ll talk about how Sanuk is doing. But Deckers management say some interesting, perhaps even insightful, things about online business and the omnichannel and I want to focus on those as well. Let’s start by getting some of the numbers out of the way.

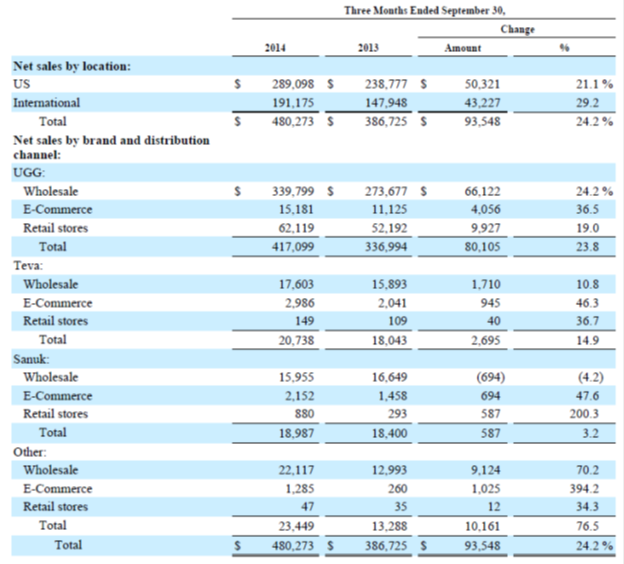

In a quarter that Deckers management describes as being historically their weakest, the company had a sales gain of 24.1%, with sales rising to $211 million from $170 million in the same quarter last year. “The increase in overall net sales was primarily due to an increase in our UGG brand sales through our wholesale channel and retail stores as well as an increase in our Teva brand wholesale sales,” says the 10Q.

But Tom George, the CFO, tells us in the conference call, that “Nearly half the upside revenue was attributed to the timing of wholesale and distributor sales and the other half with some higher than expected sales. The higher than expected sales contributed approximately $0.05 to the EPS while the other $0.21 was due to the timing of sales and operating expenses.”

So half of the revenue increase was just timing differences that don’t change their estimate of total revenue for the year. That is, the revenue was booked in the June 30 quarter instead of the September 30 quarter. But the other half of the revenue increase is from higher than expected sales.

In spite of that sales gain, the net loss rose from $29.3 to $37 million. How’d that happen?

There was a very minor decline in the gross margin from 41.1% to 41.0%. Gross profit basically rose with sales from $69.8 to $86.8 million. I guess that’s not it.

Ah, here we go. Selling, general and administrative expenses were up 21.9% from $112.6 to $137.3 million. That increase included $11 million for opening 37 new stores (they’ve got 126 stores worldwide), $4 million for marketing and promotions related to the UGG and Hoka brands, $3 million for “information technology costs,” and $3 million for ecommerce. As a percentage of sales, it fell from 66.2% to 64.9%.

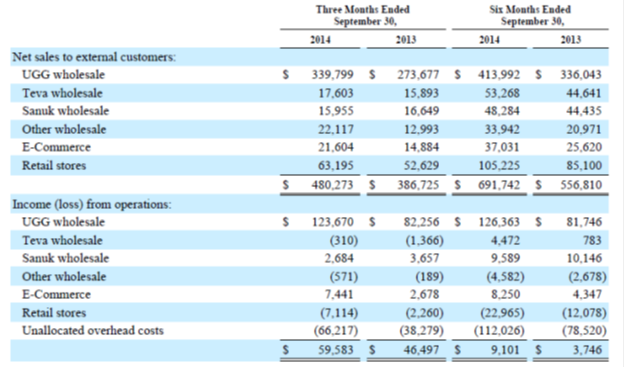

Sanuk’s wholesale revenues were $32.3 million, up 16.4% from $27.8 million in last year’s quarter. That represented 21% of Decker’s total whole sale business of $154 million in the quarter. UGG was $74 million and Teva, $35.6 million at wholesale. Deckers tells us that “Wholesale net sales of our Sanuk brand increased primarily due to an increase in the volume of pairs sold, partially offset by a decrease in the weighted-average wholesale selling price per pair. The decrease in average selling price was primarily due to a shift in product mix.” They gained $7 million in revenue in higher volume but lost $2 million due to lower selling prices.

Sanuk’s total sales for the quarter were $36 million, up 19.6% from $30.1 million a year ago. That includes ecommerce sales of $2.71 million up from $2.09 million in last year’s quarter and sales in Decker’s retail stores of $243,000, up from $22,000. We’re told in the conference call by President and CEO Angel Martinez that, “Sanuk had a strong quarter due in large part to the continued success of women’s sandals, most notably the Yoga Sling Series.” The brand is also being expanded into “…the broader selection of casual shoes and boots that can be comfortably worn during colder weather.”

He talks further about this in response to an analyst’s question. “…when we acquired that brand, the brand really was 70% men’s, 30% women’s. It was primarily distributed in surf shops and actions sports distribution. And we knew that the gender profile of the brand would need to alter significantly, if we would to have any hope of selling product in department stores for examples. So one of the things we are seeing with Sanuk is a major transition to a much more compelling women’s product offering.”

Even though its revenues are the smallest of Decker’s three biggest brands, Sanuk’s operating income, at $6.9 million, was larger than that of either UGG or Teva which, respectively, had operating income of $2.7 million and $4.8 million. That’s an operating profit margin of 21.4% for Sanuk compared to 13.4% for Teva and 3.6% for UGG.

In what can only be acknowledged to be a blinding glimpse of the obvious, I’d say Deckers needs to get that operating margin for UGG up. I suppose they are as the UGG brand had an operating loss of $510,000 in last year’s quarter. Decker’s marketing spend has increased from 5% to 6% of sales, with the majority “…being directed towards the UGG brand with the incremental dollars going towards the combination of digital programs and tactics aimed at broadening brand awareness and driving traffic to our direct-to-consumer channel.”

We’re also told that, “The increase in income from operations of Sanuk brand wholesale was primarily the result of the increase in net sales offset by a 5.1 percentage point decrease in gross margin as well as increased operating expenses of approximately $500. The decrease in gross margin was primarily due to a shift in sales mix as well as an increased impact from closeout sales.”

As you recall, when Deckers acquired Sanuk In July of 2011, there were some big contingent payments required. The last year of the earn out is calendar year 2015 and that earn out will be 40% of Sanuk’s gross profit. Deckers has a long term contingent liability of $28 million booked for that. There was an earn out due and paid in 2013 (I think it was less than 40%- maybe 35%), but there is none due in 2013.

Meanwhile, Deckers ecommerce revenue rose from $10.7 million to $15.4 million. But operating income for that segment fell from $1.7 million to $809,000. Retail store revenues rose 29.4% from $32.5 to $42.0 million but the operating loss on those retail operations climbed from $9.8 million in last year’s quarter to $15.9 million.

The balance sheet remains in pretty good shape, though current ratio has declined just slightly and total liabilities to equity is up a bit compared to year ago. I’d note that they managed to reduce their inventory very slightly even as sales rose even while bringing some $17 million in product in early due to concern about a West Coast port strike. Cash is up a bunch from $49.1 to $158 million.

Given the increase in cash, I find it interesting that after the June 30 balance sheet date, they took a mortgage on their corporate headquarters for $33.9 million. They expect to use those proceeds “…for working capital and other general corporate purposes.” I’m not clear why they did that.

Okay, on to interesting omnichannel stuff.

Dave Powers, Decker’s President, Omni-Channel, tells us that total direct to consumer (DTC) was up 33% in the quarter compared to the same quarter last year. But that includes 37 new retail stores and, as we’ve already noted, the loss from their retail stores was larger than in last year’s quarter.

Comparable DTC sales were up 10%, but that included a 39% increase in e-commerce sales and a “…low single-digit comparable store sales decline.”

As I’ve discussed a few times before, the holy grail of e-commerce is when the brick and mortar and online activities support each other. The sum has to be bigger than the parts or the rather significant investment in omnichannel activities just doesn’t make sense. Right now, we see Decker’s brick and mortar comparable store sales down, while e-commerce is up. How do you know when your e-commerce isn’t cannibalizing your brick and mortar?

Deckers knows this is important. Dave Powers says, “We now know that brick-and-mortar locations fuel e-ecommerce and vice versa. And we believe that a portion of our e-commerce growth is fueled by our increasing store base. We see the internet UGG program and similar omni-channel initiatives providing increased contribution to overall DTC comps going forward as we further tie our stores and website.”

He goes on, “The key next step of our omni-channel evolution will be the opening of a smaller concept omni-channel store in Tysons Galleria this fall. That will feature new in-store web technology such as interactive displays and the ability to reserve online and pickup in-store.”

President and CEO Angel Martinez notes that their average cost to build out stores is down 30%. He doesn’t attribute that all to smaller stores and omni-channel related stuff, but I imagine it’s had some impact. In another comment, he notes that stores may no longer need the back room. Obviously, that’s omnichannel related and has implications for further reducing real estate costs.

The devil, as always, is in the details, and here are a few of those. They are rolling out something they call Infinite UGG which “…gives us the ability to offer our retail customers every skew available from the UGG brand to our in-store POS system…Our UGG by You customization program will include additional files and design details for the consumers to choose from such as the popular daily bow and daily button…we’re also extending retail inventory online or RIO, a new tool launched this past spring in select stores in North America and EMEA advance of the fall and holiday selling season. RIO provides customers with visibility into store inventory, helping them to efficiently locate the product they want prior to visiting the store.”

From what I know, this isn’t unique to Deckers, but it certainly feels to me that they are doing the right things. CEO Martinez talks about this from a more strategic perspective.

“…just a few short years ago we were a wholesale vendor that delivered product twice a year and our success was largely driven by how well buyers, wholesale buyers responded to our collections at industry tradeshows. The consumer had very little influence in shaping our future direction. This dynamic has been turned completely upside down. The consumer is now the gatekeeper and we’ve transformed our business model to not only adapt to the new retail paradigm but also to thrive and to grow.”

“We now drop product more than 10 times a year and communicate with consumers on a much more frequent and personal basis. This constant flow of information is reshaping our growth strategies including our product development and store expansion plans, as we now have much better insight into pinpointing demand and directing capital towards what we believe will be high return, high productivity locations.”

Dave Powers adds to this when responding to an analyst’s question:

“So we’re starting to think about the stores as not just the store in a four-wall P&L but a store that impacts the overall macro environment of our brand in that metro area. The inverse of that is that we have the ability now through analytics and increasingly CRM and loyalty programs through e-commerce to better target customers in those metro areas we know where they are. And we can send them through merchandising and marketing initiatives digitally back to the store.”

Sorry for the long quotes, but I couldn’t say this important thing any better. And I could go on with more quotes, but I think you get the picture. Deckers is making a big bet on the omnichannel. Well, who isn’t? But their conception seems particularly well thought out.

When Deckers first bought Sanuk, I suggested that they didn’t quite know what they’d bought and what to do with it. Given the price they paid, I have to believe they are not completely happy with the results to date. To justify the purchase price, they have to be able to take it from a quirky surf, beach, action sport brand to one that will sell well in broader distribution. But of course they have to do that without losing the quirkiness.

Quite a challenge and the 5% decline in Sanuk’s gross margin during the quarter gives me pause. So here we are again. Can a brand owned by a public company grow fast enough to satisfy Wall Street without damaging the brand? I hope the crew at Sanuk is following what Skullcandy is trying to do.