Zumiez reported a solid August 3rd quarter, and their balance sheet remains rock solid. They had to deal with the same pandemic issues as everybody else, and their responses were similar. But what we are reminded of in the 10Q and the conference call, like for the 50th time, is Zumiez’s is confidence in their culture, their balance sheet, that ecommerce and brick and mortar as one channel, and that their data systems and trade area concept coupled with instore ecommerce fulfillment offers them an advantage as retail changes.

The faster things change, the bigger the advantage may be. First the numbers. Then a little deeper dive into some of the things they don’t quite say but are maybe implying that you should think about.

First the Numbers

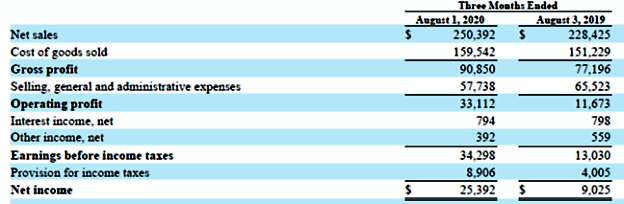

Here’s the chart showing Zumiez’s financial results for the three-month periods we’re comparing. All numbers in thousands of dollars.

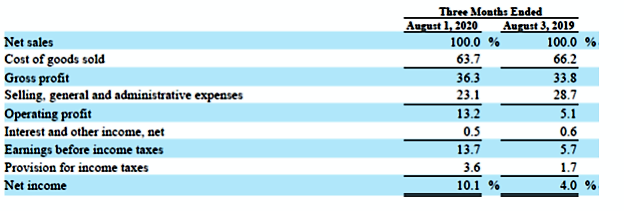

This second chart shows the percentage changes in the same numbers across the quarters.

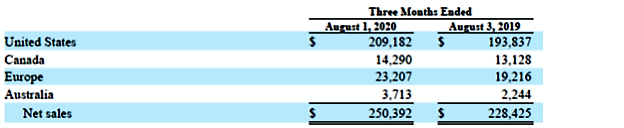

This third and last chart shows sales by geographic region for the two quarters. In thousands of dollars of course.

Zumiez ended the quarter with “…720 stores; 607 in the United States (“U.S.”), 52 in Canada, 49 in Europe, and 12 in Australia.” Zumiez began to have virus related store closures in mid-March. “We began gradually re-opening physical stores at the end of the first fiscal quarter and into the second fiscal quarter. At the end of May, we had 68.4% of stores re-opened. At the end of June, we had 96.0% of stores re-opened. During July, we closed 69 stores in California and Australia and continued to have a varying number of up to 13 stores closed and re-opened, globally, as a result of governmental orders and COVID-19 precaution. As of August 1, 2020, 645 of our stores, including 538 in the U.S., 52 in Canada, 49 in Europe, and 6 in Australia, which represents 89.6% of our total count, were open and operating.”

Even with the closures, net sales grew 9.6% with, as you can see above, all regions growing. Comparable store sales were up 20.1% and ecommerce sales by 122.2%.

Even though Zumiez thinks of its brick and mortar and ecommerce as one sales channel, I’m glad to see them distinguishing between the growth in the two. Seems to me that they had stopped doing that for a while.

The gross profit margin was the result of “…a 170 basis point increase in product margin, a 160 basis point decrease in store occupancy costs, a 50 basis point decrease in distribution costs, and a 20 basis point decrease in inventory shrinkage. This was partially offset by a 160 basis point increase in web shipping costs due to increased web activity…”

You can see that SG&A expenses declined by 11.9%. “The decrease was primarily driven by a 240 basis point decrease in our store wages, 100 basis point leverage in other store costs, a 70 basis point decrease due to governmental payroll credits, a 70 basis point decrease in corporate costs, a 40 basis point decrease in corporate wages, a 30 basis point decrease in annual incentive compensation, and a 20 basis point decrease in national training and recognition events.”

Note that the decline is largely the result of Zumiez’s response to the virus, including 0.7% from government payroll credits.

As indicated earlier, the balance sheet is solid. No long term debt. Cash and marketable securities rose from $180 million at the end of last year’s quarter to $290 million at this quarter’s end. Cash generated by operations almost doubled from $35.2 to $62.0 million. Inventory declined from $151 to $127 million. That’s not entirely a good thing, as they indicated they were losing some revenue because of inventory shortages.

What They Don’t Quite Say

In his initial conference call comments. CEO Rick Brooks talks about their “…difficult near-term decisions around our expense structure in order to weather this crisis and emerge in a position of strength.” Lots of industry companies- companies in general actually- are making those kinds of decisions. Often the virus has been the excuse to take actions that should probably have been made before but were just a little too traumatic. I’m seen a lot of that in turnaround work.

But Rick does not go on to say, “These expense reductions are temporary, represent critical business investments, and will be reversed when this whole virus can of worms goes away.”

He does go on to say, “These results in this environment underscore the strength of our brand and culture, and speaks to the ability of our business model to adapt to change.” Some paragraphs later he says he expects the environment to accelerate further consolidation. Then he closes his introductory remarks saying, “We must be smart in how we navigate the business challenges, while also looking for long-term strategic investments that will set us up for the future. These include great real estate opportunities, new tools within our omnichannel formats and other strategic investments to support the next era of intimacy and now with our customers. The strength in our position can be a significant advantage in these times.”

Let me interpret and maybe try to mind read a little and tell you what I think I just heard Rick say.

- Wow! We knew about most of these trends, but who knew they’d happen this quickly.

- Really good we’ve got the balance sheet, culture, systems, and resulting flexibility to move fast.

- I wouldn’t wish this mess on us or anybody else, but I think it might just work out for Zumiez.

- I wonder if we need to change how we think about brick and mortar over the longer term. Maybe we aren’t maxed out in the U.S. if there are quality locations at lower prices.

- Can’t wait to see what the algorithms in our shiny new data systems tells us.

- I wonder just what part of those expenses we cut really need to be restored. Pretty sure we’ll have to eventually pay $41.5 million for deferred landlord payments, delayed inventory, extended vendor terms and deferred payroll tax payments. Oh well. But some of the other cuts we’re going to have to think about.

I won’t try and channel CFO Chris Work, but he does tell us a few intriguing things. First, that they are really focusing on the trade area concept, “…looking at stores and web to serve our customers and believe that they definitely work together.” They don’t want one more unit then they need in any geographic area. The trade area idea is very, very dynamic. This is the thing they don’t quite say. Zumiez is in the early stages of taking advantage of it and don’t know exactly how it is going to work out.

Of their bottom 20% of stores, they can get out of 75% if they want to in the next three years. That’s a lot of short to medium term flexibility. As Zumiez gets better and better at figuring out which inventory to have in what trade area (or store) by what date and as the closing of retail stores and consolidation of malls continues, Zumiez is going to have a remarkable chance to maximize a trade area’s revenue while minimizing expenses.

That’s me talking. That’s what I think they are shooting for.

At the highest level, Rick and Chris always tell you exactly what they are going to do. But they tell you so softly and gently that you’re lulled into not thinking too hard about the implications. Especially if you just listen to the conference call. When I listen, rather than read, I feel like a college student in a lecture I know is important but that I want to end.

There’s a lot of turbulence underneath the calm surface of the Zumiez’s lake. I’ll try and get out my scuba gear every quarter.